Why we built Quartz

Most people think of their financial lives as simple. A salary comes in, bills go out, a pension grows somewhere in the background and, if they're disciplined, some savings accumulate along the way. Because of that simplicity, many people treat their savings rate as the only financial variable they can control. But that is not the case.

Approaching wealth building through first principles and, ignoring taxes for a moment, one’s wealth is the result of:

- How much you earn (income)

- How much of it you save (savings rate)

- What those savings earn over time (rate of return)

Assuming that we’re all doing what we can to grow our income, we’re left with the last two. And they behave very differently.

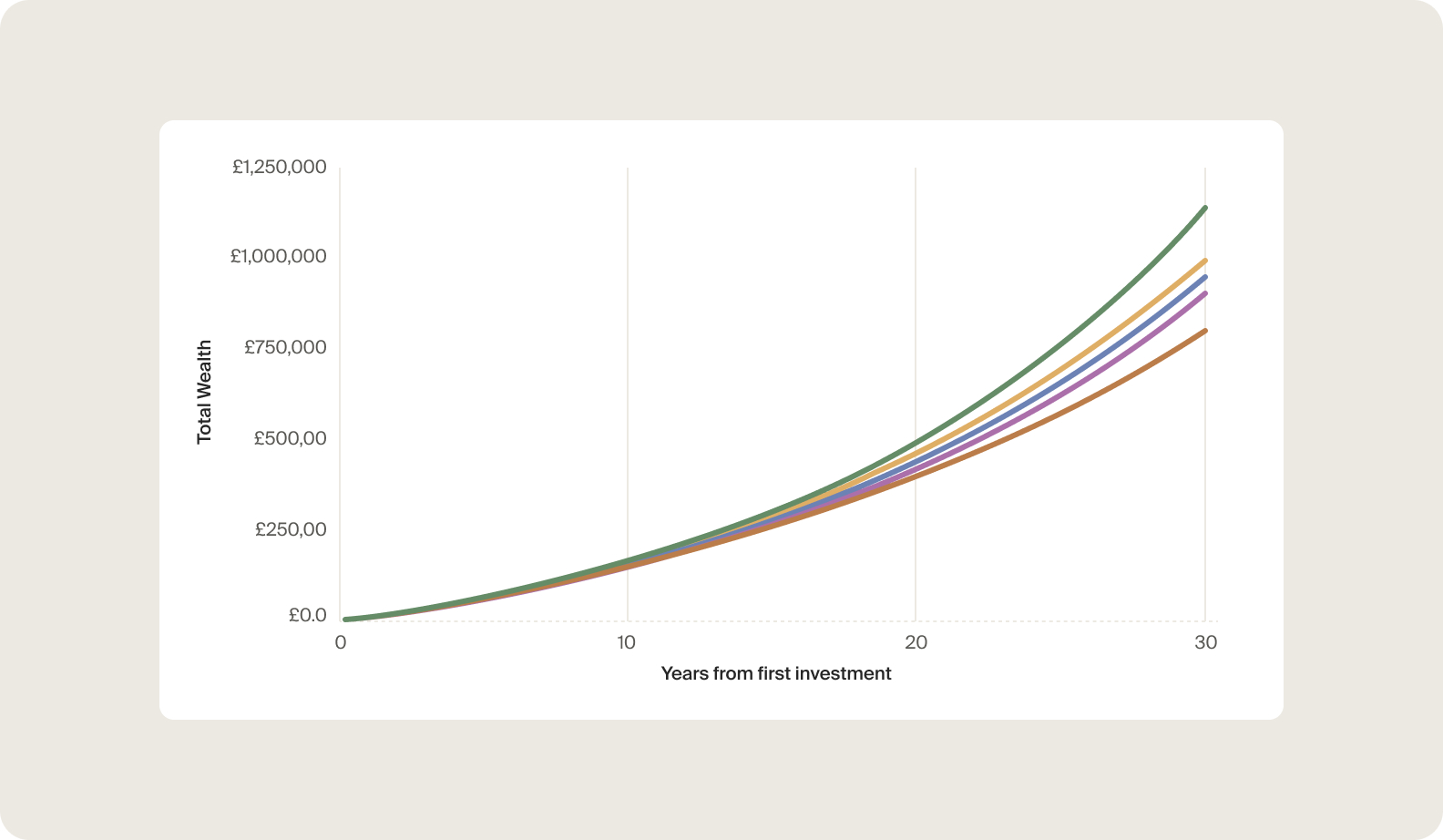

- Savings rate affects future wealth linearly.

Adding 1 percentage point to your savings rate surely helps but comes at the expense of your consumption and it’s one for one. - Rate of return affects future wealth exponentially.

Adding 1 percentage point to your investment return reshapes the curve of your entire financial future and this impact grows further every year. It’s called compounding. Or the 8th wonder of the world.

Assumes a £60,000 yearly income and monthly contributions.

Ok, but isn't that just for the very rich?

Having established that investing is, at least, as important as saving, it begs the question of how much the median individual can expect and should worry about it.

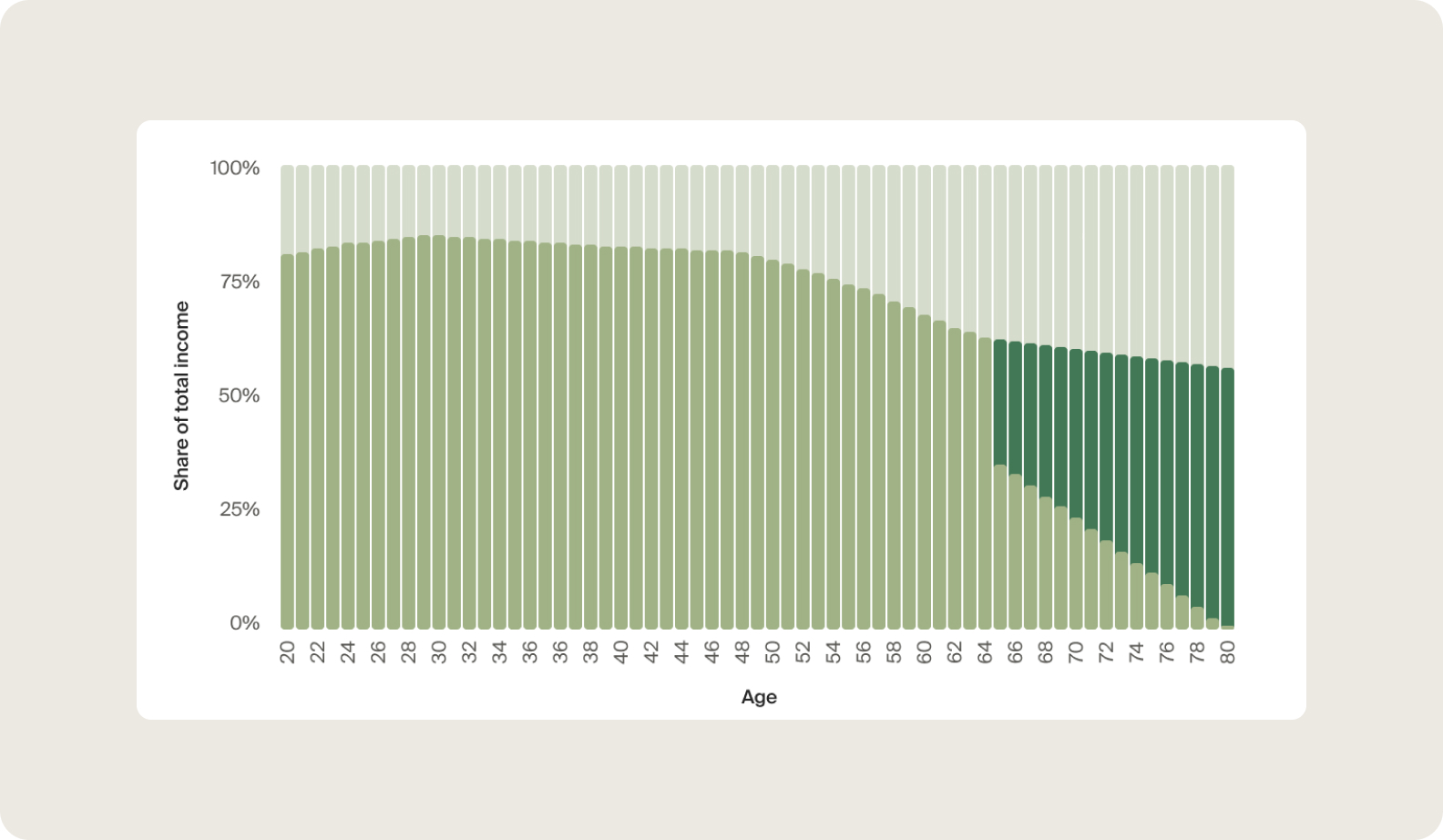

According to UK income data, the median individual earns roughly 80% of their total income from salary and other employment-related sources. The remaining 20% comes from property income, interest, dividends, pensions, and other forms of capital income, with more than half of that sitting in pensions1.

Well, 20% is already meaningful but the real story is in the distribution: Wealthier individuals have a much higher share of capital income vs salary and other income. But so do older people and, while we might not be all on the path towards being ultra wealthy, we’re all certainly going to get older. And yet, most people put relatively low importance on something that will be so determinant in at least a third of their lives.

Citing Thaler (2017 Nobel in Economics), “People are often more like Homer Simpson than Mr. Spock when it comes to financial decisions” and “asking individuals to manage their own retirement savings is akin to asking them to build their own cars”. Behavioral biases aside, there is one point that is painstakingly clear: Good “wealth mechanics” are expensive and traditional advisory models were never designed to serve the median individual.

We decided to ask why not?

Why shouldn’t everyone have access to the kind of financial capability that enables them to benefit from economic growth and build a stronger future? We think it should be a given. Yet, it remains reserved for a wealthy minority, and is as much of a mindset issue as it is a structural microeconomics problem.

The reality is that traditional wealth managers and financial advisors operate with a cost structure dominated by people: 60–70% of their total cost base is headcount2. Their service model is built around human time, face-to-face interactions, manual research, and fragmented tools. As a result, it scales poorly. Each new client adds meaningful marginal cost, which forces the industry into a simple trade-off:

- Personalised advice at a premium price, or

- Standardised products with minimal guidance

We believe that trade-off no longer exists

At Quartz, our generative AI model allows us to deliver deeply personalised financial intelligence at a fraction of the traditional cost. It brings together the three pillars of high-quality insights:

- Deep understanding of the individual

We don't forget your goals, your preferences, your financial behaviour. We spot patterns in your portfolio that would be invisible to others and adapt our insights as your life evolves. - Institutional-grade awareness of markets

You might miss a headline or be busy with your day job to stay fully up to date. Our model ingests market data, macro trends, news flows, and analysis continuously and translates that into context-specific insight for you. - Personalised insights delivered the way humans think

Where most technology providers fall short is in how they deliver insights: it feels generic, transactional, or impersonal. We're rebuilding this layer from the ground up, making it multimodal, conversational, and intuitive. At Quartz, you can literally talk to your portfolio, and it might just talk back!

If you’re curious about it, you should join the waitlist

People shouldn’t have to choose between living their lives and managing their wealth. Most people don’t have the time, or the desire, to become financial experts. But that, or the wealth you start with, shouldn’t determine whether you can participate in economic growth.